FOREIGN companies invest in India or elsewhere to earn profits. Foreign companies lobby to enter in India to exploit its market. If they make profits, it is expected that they pay tax on the profits in India and when they exit the investment, pay tax on the capital gains. Of course, these rights of taxation can get modified in terms of tax treaties if any. In the context of the retrospective amendments in the Vodafone case, there is no question of any tax treaty and the issue has to be understood in terms of the domestic law alone.

In the nineties, foreign telecom operators were allowed to invest in India subject to certain caps. One player who entered the Indian market was Hutchison. It earned handsomest profits from India and then exited. On exit, it was expected to pay tax on the capital gains made. Vodafone, the largest telecom player in the world wanted to enter India. It bought out Hutchison. Everyone knew that there will be liability to capital gains. Efforts were already on through the jugglery of holding companies, subsidiary companies, companies incorporated in tax havens, quasi havens to eliminate this liability. Fixers, tax planners, tax experts, everybody got into the act. They gave a verdict that there will be no tax on the capital gains. The Indian Revenue warned Vodafone that it should not remit money without deduction of tax at source. Confident of its financial muscle and pelf, Vodafone royally ignored the warning and went ahead with the transaction and made the payment to Hutchison. Subsequently when it was slapped with a demand notice, a campaign started against the Indian Revenue. Experts of different hues opined against the Revenue's actions. Vodafone's challenge to Bombay High Court failed. The High Court took a common sense view and held that the real target of the acquisition was always the Indian telecom assets with the licenses to operate in India and it was never a question of transfer of a share of a company several tiers away in Cayman Islands.

Certain sections within the government were not happy at the developments and were perhaps concerned that the action of the Revenue will drive foreign investments away. Be that as it may, the Supreme Court chose to go by the form of the transaction rather than substance and also chose to differ from a larger bench's formulation regarding tax avoidance. The government moved a review petition against the Supreme Court decision, which was also promptly dismissed. The correctness of the Supreme Court decision has now been questioned by one of the Government of India's own law officer as also by some retired judges of the Supreme Court. It is true that most of the pink press and lobbying groups expressed happiness with the Supreme Court decision. It was quite possible for the government to accept the decision and let the matter rest. This course of action would obviously have had repercussions on other similar pending cases. It would also have repercussions on the revenue. Presumably therefore, the government, after due deliberations, decided to overturn the decision through legislative action. The decision of the court was exceptional and required exceptional measure. (For an analysis of the Supreme Court decision, see Vodafone Judgment - Part 1 + Part 2 + Part 3)

The Finance Bill, 2012 contained the necessary proposal in this regard. If the intention of the legislature was never to give exemption in Vodafone type of cases, naturally the amendment had to have retrospective effect with effect from the time the particular provision was introduced in the Act, which in this case was from the beginning i.e.1.4.1962. In India, there is a time lag between the presentation of the Finance Bill and the passing of the Act. There are many instances of a proposal mooted in the Finance Bill being subsequently dropped as a result of the debates and discussions that follow the presentation of the Finance Bill. It is true that there were criticism of the proposal from business groups against the amendments, particularly against the retrospective nature of the provisions.The academic circles were somewhat divided. The civil society groups like Tax justice network was largely in favour of the proposal. Ultimately, the Parliament of India passed the Bill containing the retrospective provisions

What transpired thereafter is a theatre of the absurd and perhaps can take place only in India.The provision relating to GAAR having got the goat of the foreign investors, they succeeded in brainwashing a section of the Indian media that by investing in India they were doing an altruistic service to the country without ever mentioning that it is India that offers its huge market for them to exploit. Certain influential peoples also started making noise that GAAR and the retro taxation were the root of all evils and had to be junked. The then Finance Minister having moved to the highest office of the Republic, the Prime Minister constituted an expert committee headed by Dr. Shome to finalize the guidelines that were in the process of being put up by the Tax Department consequent to the passing of the Finance Act and incorporation of GAAR in our domestic law. The expert committee however, ended up by recommending the postponement of GAAR itself besides suggesting a number of steps to dilute its effects. We have already discussed the committee's suggestions in this regard in earlier episodes.

As the committee was examining the GAAR issue, which, in itself is a serious issue, the committee was saddled with additional responsibility to “Examine the applicability of the amendment on taxation of non-resident transfer of assets where the underlying asset is in India, in the context of FIIs operating in India purely for portfolio investment.” This was in the context of the FIIs threatening to pull out of India. The committee was asked to give its report post haste within one month. On the 1 st of September, the terms of reference of the committee were, however, further expanded to examine “the applicability of the amendment on taxation of non-resident transfer of assets where the underlying asset is in India, in the context of all non-resident taxpayers.” The committee was to give the report within one month.

The committee was thus asked to examine the applicability of the amendment in section 9 and elsewhere to non-residents investing in India. As per the language of the terms of reference, perhaps what was required was for the committee to examine the different fact situations in which the liability of the non-residents arises from the application of the amendments. The committee not only gave its views on the capital gains on indirect transfer but also went into the desirability of retrospective amendment itself. It came up with the now famous quotable quote that retrospective amendments should be resorted to in the ‘rarest of rare' cases and gave a four-point action plan in this regard. The committee also questioned the clarificatory nature of the amendments despite the fact that the then Finance Minister explained on the floor of the house that the proposed amendments were indeed clarificatory in nature.

It is true that for the retrospective legislation, the government got flak from industry associations including the foreign ones. Ministers from the UK and the Treasury secretary of the USA also got into the act. All this, after sovereign India's sovereign Parliament passed a legislation after due deliberations. It is but natural for vested interests to howl and protest at India's alleged perfidy. But, is India alone in taking steps against offshore tax evasion and exploitation of indirect transfer route? Have no other nations taken such steps?

The expert committee has educated us about the fact that countries such as Paraguay, Peru and what have you, have prohibited retrospective amendments. The system of taxation of some of these countries may not at all be comparable with us. Generally, commentators never tire of comparing India with China. It is therefore surprising that nobody talked of the measures that China took to deal with similar situations.

In this article, I therefore intend to discuss two Chinese cases to show how the Chinese deal with its foreign investors and how these foreign investors react when they deal with the Chinese.

The Chongqing case:

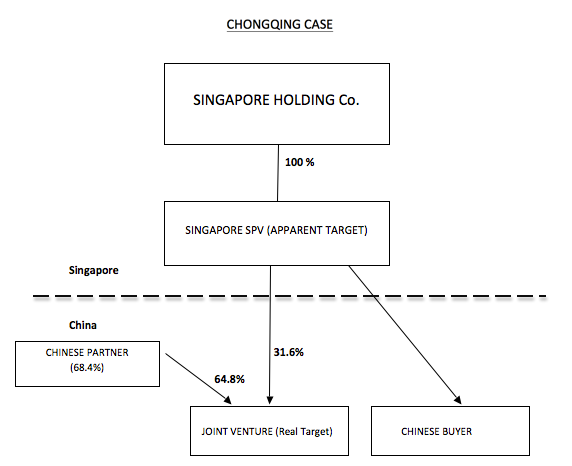

The first one is known as the Chongqing case and internationally there have been comments that in taking action in this case, the Chinese tax authorities were largely inspired by the action of the Indian Revenue in the Vodafone case. This case was posted in November 2008 even before circular no 698 relating to indirect transfer was announced by the Chinese tax administration.

In this case, a Singapore company held 100% shares of another Singapore subsidiary, the apparent target of acquisition. This company, in turn, held 31.6% of the equity of Chongqing Company, which was the real target. The Singapore Company sold its stake in the apparent target Singapore Company to a Chinese buyer. Describing the case, Stephen Nelson, Head Tax Practice, King & Word PRC lawyers mentions: “Capital gains would not be subject to withholding tax in China for an offshore transaction such as this. Nevertheless, perhaps having studied the handling of the Vodafone transaction by the Indian authorities on very similar facts, the Chongqing tax authorities challenged the transaction as a tax avoidance arrangement and denied the existence of the Singapore target company based on the following rationale:

-The Singapore target Company was not engaged in any operating activities except for holding 31.6% equity interest in the Chongqing Company.

-In substance, the equity transferred was in fact the equity interest in the Chongqing Company.” (Source: Tax Risk Management edited by Sander)

One can perhaps argue that in this case the ultimate investor was Chinese. That fact alone should not make any difference. However, there are more such cases from the Chinese stable. Obviously, none of the ‘stakeholders' would ever present these cases before the expert committee. Let us analyse another case in this regard.

The Carlyle case:

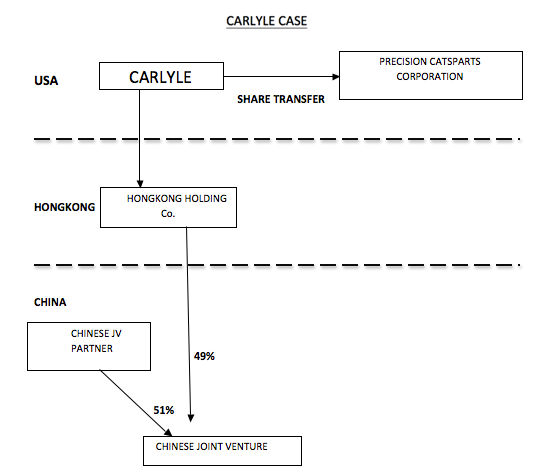

The name involved in this case is a big name in private equity – the Carlyle group which operates also in India. Carlyle had a subsidiary in Hong Kong, which had invested USD 80 million private equity in 2007 and owned 49% interest in a joint venture in one Yangzhou Chende Steel Tube Co Ltd in the Jiangsu province. In 2010, Carlyle sold off its stake to one Precision Castparts Corporation for USD 350 million resulting in substantial gains to Carlyle.

The local tax authority in Jiangdu came to know of Carlyle's intention to transfer its interest in the joint venture at the beginning of 2009. Thereupon, the Jiangdu Tax Authority formed a team to track the potential transfer. At the beginning of 2010, it came to the notice of the Jiangdu Tax Authorities that an indirect transfer had taken place outside China. Much like the Indian authorities, they asked for the information about the transaction from both the buyer and the seller. They also asked for a copy of the share transfer agreement. Again, like the Indian tax authorities and probably taking a cue from them, the Jiangdu Tax Authorities visited the website of the buyer's US parent company to find out more information about the transaction.

On the basis of the information so gathered, the Jiangdu Tax Authorities found that as is the practice in the private equity industry, the Hong Kong Company had no employees, no assets, no liabilities, no other investments, and no business operations. In effect, very much like the Cayman Islands Company in the Vodafone case, it had no economic substance. The Jiangdu Tax Authorities therefore held that the transfer of the Hong Kong Company was in substance a transfer of the Chinese joint venture company and hence should be subject to Chinese withholding tax. [Source: China: taxing offshore transactions – Julie Zhang]

As in the case of Vodafone, Carlyle argued that it was not be obliged to pay any tax in China since the buyer, the seller and the immediate target company were all located outside China. However, the Jiangdu Tax Authority rejected this argument. On approval of the State Administration of Taxes (SAT), the Jiangdu Tax Authority asked Carlyle to pay China withholding tax on the transfer.

Note that there is no High Court, Supreme Court, no lobbying and bad mouthing of the Chinese tax administration. The State Administration of Taxes, an administrative body-like the CBDT in the Indian context, gave the approval to the local tax administration. It is reported that after several rounds of negotiation, Carlyle filed a tax return and settled the payment of CNY173 million on 18 May 2010

Let us contrast this with the reaction in India. Even when Vodafone itself was making a provision in its accounts for the possible outgo of billions of USD on account of its tax liabilities in India, the expert Committee gives a report which, if implemented will absolve Vodafone of all its liabilities. And of others who have already complied with the Revenue's directions.

One can argue that there was no retrospective legislation in China. But, the recourse to retrospective legislation would not have been necessary in the first instance if we could act decisively. Retrospective legislation has to be resorted to when the interpretation put by the Courts are such that were not at all intended by the lawmakers. True, it should not be resorted to in a routine manner. But, there is no reason to restrict retrospective legislation to correct anomalies when required, particularly when no body can claim clairvoyance.

Mr.Bishwajit Bhattacharya in his book ‘My Experience with the Office of Additional Solicitor General of India' gives examples of cases where retrospective amendments have been resorted to by the Government. He points out that in Municipal Committee, Patiala v. Model Town Residents' Association, (2007) 8 SCC 669: AIR 2007 SC 2844: 2007 AIR SCW 5164 - 1-8-2007 a two-Judge Bench of the Supreme Court comprising Mr. Justice S.H. Kapadia and Mr. Justice B. Sudershan Reddy held, inter-alia, as follows:

"...in the above judgment, the High Court directs the State Legislature to amend the law relating to determination of annual value by clarifying that any such amendment shall not be retrospective. We have serious reservations regarding such a direction. It is not open to the High Court under article 226 of the Constitution, particularly in the matter of taxation directing it not to amend the law retrospectively. Such a direction is unsustainable, particularly in a taxing statute. It is always open to the State Legislature, particularly in tax matters, to enact validation laws which apply retrospectively. The High Court cannot take away the power of the State Legislature to amend the tax law retrospectively. The basis of the law can always be altered retrospectively."

Mr. Bhattacharya adds: ”It is therefore clear as crystal that in taxing statutes Parliament's power to amend the law retrospectively is unquestionable.”

In contrast with the Chinese reaction, when the Indian tax administration goes after tax avoiders and evaders, instead of standing by them, a part of the administration seems to be actively trying to undermine its authority. Fat lot of hope then that India will ever be able to increase its tax GDP ratio to any appreciable level. |